In the third article in this series, we cover Asset-Referenced Tokens (“ARTs”), one of the three categories of tokens covered by MICA (i.e., e-money tokens and other tokens).

An ART is a type of crypto-asset that is not an electronic money token and that purports to maintain a stable value by referencing another value or right, or a combination of the two. This could include one or more official currencies, one or several commodities, one or more crypto-assets, or a combination of such assets[i].

The requirements that are currently proposed are designed to create a robust regulatory framework for ARTs and to protect investors in these crypto-assets by:

- Ensuring that ARTs are issued by reputable and well-regulated entities.

- Ensuring that ARTs are backed by the established asset reserves and that investors are protected, even if the issuer becomes insolvent.

- Helping investors make informed investment decisions.

- Helping investors track the performance of the ART

- Ensuring that the issuer is operating in a sound and transparent manner.

It is important to note that the requirements for ARTs under MiCA are still under development[1] and may be subject to change.

Requirements applicable to ARTs

|

ART Issuer Requirements

|

|

|

White Paper[v] |

|

|

Marketing Communications |

|

|

Publication[vii]

|

|

|

Transparency Requirements[viii]

|

|

|

Governance Requirements |

|

|

Reporting Obligations with Competent Authority |

|

|

Significant ARTs

|

|

Custodians of ARTs:

Article 36 requires issuers to constitute and maintain at all times a reserve of assets which will be legally segregated from the issuers’ estate, as well as from the reserve of assets of other ARTs, in the interests of the holders of ARTs in accordance with the applicable law. One of the consequences would be that issuers' creditors have no recourse to the reserve of assets, particularly in the event of insolvency. The reserve assets are required to be held in custody and such a service can be provided by a CASP which provides custody and administration of crypto-assets on behalf of clients.

The custodian of an ART must be a legal person that is different from the issuer of the ART. This means that the custodian cannot be the same company as the issuer. The custodian must have the necessary expertise and market reputation to act as custodian of the reserve assets. They must also keep records of the reserve assets and provide regular reports to the issuer.

The appointment of the custodian must be evidenced by a contractual arrangement. This contract must specify the rights and obligations of the custodian, as well as the procedures for managing the reserve assets.

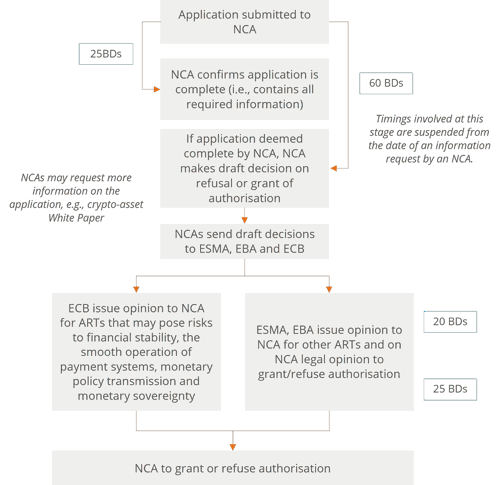

MiCA Timelines: ARTs issued by legal person.

The diagram below provides an overview of the timelines involved in an assessment of the application for authorisation as per Article 20:

What else are we to expect?

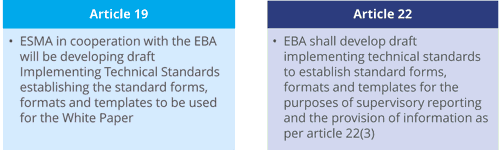

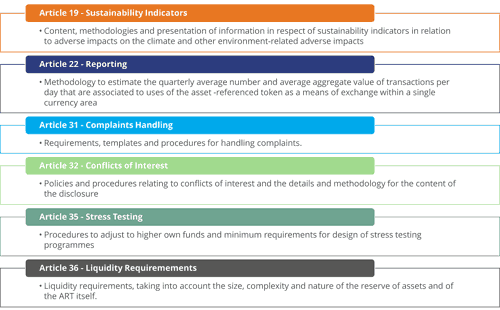

Implementing technical standards

Regulatory technical standards

As it stands, the European Securities and Markets Authority (“ESMA”) and the European Banking Authority (“EBA”) are set to release different Regulatory Technical Standards (”RTS”) specifying key items on several topics:

Guidelines

Follow our Global Regulations Tracker

Over the coming months we will release a series of articles that delve deeper into MiCA through expert opinion and analysis. Make sure to read our articles on MiCA and understanding crypto-assets.

Apex Group Can Help

We can help you stay compliant with the latest regulations and protect your business from financial crime. Get in touch for further information on:

- Crypto/Virtual asset/VASP-CASP licensing

- Crypto-assets Due Diligence services

- Crypto AML compliance support

- Crypto Compliance Training

[1] At the time of this article

[i] Article 3(6)

[ii] Other undertakings may issue ARTs only if their legal form ensures a level of protection for third parties’ interests equivalent to that afforded by legal persons and if they are subject to equivalent prudential supervision appropriate to their legal form.

[iii] Article 16(3)

[iv] Reference should be made to Article 17 in relation to the requirements applicable to credit institutions which wish to issue ARTs.

[v] Regulatory Technical Standards are to be expected. Furthermore, Regulatory Technical Standards will be developed.

[vi] In the case where the ART is also offered in a Member State other than the issuer’s home Member State, the White Paper shall also be drawn up in an official language of the host Member State or in a language customary in the sphere of international finance.

[vii] Article 28

[viii] Article 30

[ix] Article 36